In Portugal, both the employee and the employer pay taxes based on gross compensation. In addition to such taxes, the employer is subject to fulfilling the obligations regarding employees’ mandatory benefits.

BASE SALARY

The base salary, also known as gross or gross salary, is the main part of the costs that a company has with the worker. It is also based on this amount that other costs are calculated, such as the amount paid to Social Security. The gross remuneration is paid in 14 instalments (the 13th and 14th months - corresponding to holiday and Christmas allowances).

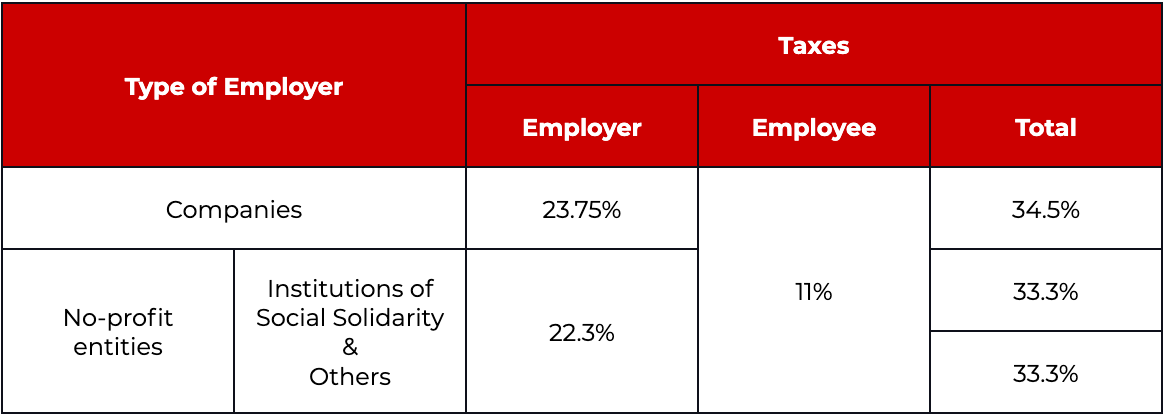

SINGLE SOCIAL TAX - SOCIAL SECURITY

The amount paid to Social Security is coming both from the employer and the employee, although for the latter the withholding is withdrawn from the monthly base salary.

In most situations, the contribution rates to be applied are shown in the following table:

Source: Social Security Official Website

WORKER’S COMPENSATION INSURANCE

Worker's Compensation Insurance is mandatory for any company, without exception. Bonuses vary depending on the risks implicit in the activity carried out by the worker.

On average, the labour insurance premium is 1% of the income to be insured. This is, therefore, an important part to consider when calculating the total cost of an employee.

MEAL ALLOWANCE

The meal allowance is considered a social benefit and is paid for by the vast majority of companies. It is not mandatory by law, depending on the collective labour agreement applicable, but it is usually paid as it is not subject to taxation, according to the following rules:

-

If the meal allowance is paid in cash or bank transfer and does not exceed €6.00 per day, it is exempt from Social Security and IRS contributions.

-

If the meal allowance is paid by a prepaid meal card, the maximum amount exempt from taxation is €10.20 per day.

Any amount exceeding the above-mentioned is subject to Social Security contributions and Personal Income Tax.

OTHER COSTS

In addition to the costs listed above, there are other mandatory costs related to the occupational health and safety audit, the employee yearly medical exam, and professional training (the employer must provide 40 hours of accredited training per year to each employee, or pay them the correspondent amount instead).

There are also other, non-statutory allowances and perks that employers can offer their employees such as:

-

Transport allowance;

-

School voucher;

-

Childcare voucher;

-

Health insurance;

-

Life insurance;

-

Work from Home allowance;

-

Technical equipment;

-

Gym pass;

-

Company car

-

Work from Home Allowance (recommended and expected to be mandatory with the review of telecommuting regulations)

For additional information on employment taxes in Portugal, please download our detailed guide here or speak to one of our experts.